What Industry Should I Buy a Business In?

-

If you’re stumped on which sector to enter, don’t worry – here’s a few questions you can ask to help you reach the right decision.

Have you decided that being your own boss suits you more than the 9-5 treadmill? Once you’ve come to this conclusion, there are plenty of factors to consider.

Deciding to buy a business rather than start from scratch will have its advantages. You will find it easier to secure financing, you will be able to see a proven track record of the business and you will hit the ground running on an already existing operation.

Making sure this endeavour is a success, though, will still mean finding an industry that fits your skills, attributes and goals. You will need to spend time researching how to buy a business.

You want to be confident in the decision you make – after all, you’ll probably be plunging personal savings and a lot of time into the project. So, don’t take the commitment lightly and carefully consider the product or service that you will offer.

There are arguably three factors to consider that should take primacy over the rest when choosing the right sector.

Picking an industry in which to buy a Business, is not a decision that should be taken lightly, among the obvious questions to ponder are things like: Is this business prone to suffer more so than others during a recession? Is it seasonal, or a year round business? What are the physical and scheduling demands, am I up for it, and for how long?

Experience

An obvious starting point to consider is your career up until now. What industries have you worked in before?

You don't necessarily have to buy a business in the same sector - but it helps if there are at least some transferable skills to bring across to your next field. For instance, if you’ve worked in cafes, your experience will readily apply to the hospitality sector - i.e. bars, restaurants and, to a lesser extent, B&Bs or hotels.

There are some skills that will apply to any business that you are running. If you're a lifelong accountant, for example, these skills apply to most sectors – accounts are an unavoidable part of any business.

Your past experiences can help you draw up a shortlist. Brief stints in many industries needn’t be worse than specialising and excelling in one or two; you'll have a clearer idea of the range of fields in which you do and don't excel.

If you've always hated office environments, for instance, that can eliminate many sectors from your thoughts.

Ask yourself:

- Which industries do I have experience in?

- What skills do I have, and can I apply these to other fields?

- Which of these skills can I apply to business in general?

- Which sectors did I perform particularly well in - or poorly - and why?

- Money and risk

Beyond some of these basic, fundamental questions, it’s useful to do an inventory of your personal skill set. What’s your background? What sort of transferable skills do you have, and are they relevant to the types of businesses you are looking at.

If you have no experience in the food and beverage industry, but think that you might buy a restaurant because you think that you are a pretty good cook, you may want to think again. Putting a wholesome meal on the table for your family, and managing all of the various intricacies required of a running a restaurant, are about as similar as chalk and cheese.

Your chances of being successful are often directly affected by your exposure to, and history of working in a particular industry.

Money and risk

Some sectors are more lucrative than others. There are also some sectors that are a lot riskier than others.

Some businesses, like dry cleaners, are often safe bets but only ever generate a modest income. These are more your lifestyle businesses. Opening a restaurant, on the other hand, is a riskier venture and so you will be more likely to only go into this if you are extremely passionate about it.

Are you hoping to become very wealthy or are you more driven by job satisfaction?

Do you have an appetite for risk, or do you prefer to play it safe?

Also, take notice of commercial trends. Healthcare, tech, construction, and education and training are projected to grow for years to come.

And how much money you are willing - and able - to invest? Your budget will filter out sectors above a certain threshold - with hotels and manufacturing typically among the most expensive.

Ask yourself:

- What is my budget?

- What skills do I have, and can I apply these to other fields?

- Do I have an appetite for risk?

- What sectors are most promising in terms of future prospects?

Passions and interests

When it comes down to it, it will probably take a lot more than money to keep you excited about your business.

Being passionate about what you do will give you job satisfaction, enthuse your employees and impress customers. And all of this keeps you going during the tough times that inevitably sometimes arise.

Make a list of what you enjoy doing and the tasks you find tedious or stressful.

You might enjoy interacting with people or working outdoors; your dislikes might be working at a desk or working evenings and weekends.

This list will help you draw up a shortlist that fits your talents, personality and circumstances.

Ask yourself:

- What am I passionate about in life and what does this say about me?

- What elements of my past jobs have I loved?

-

Are there things that I don’t like that may be a barrier in certain industries?

It’s important to be realistic. There is always room for ambition but try not to choose an industry for superficial reasons - like buying a bar simply because you enjoy drinking and socialising.

And your choice needs to encompass some combination of two or three of the factors outlined above. Don't buy an online retailer, for example, because you anticipate low overheads and strong growth prospects, but you lack the requisite skills, experience or passion for what's involved day to day.

Beyond personal experience, what may just be more important is, Passion. Running a business, more often than not, requires a great deal of blood, sweat, and tears; more than most people would expect. If you are regularly called upon to dig deep, and “go the extra mile” for your business, it’s a lot easier to do so when you are dealing with a product/service, that you are sincerely passionate about. Ultimately, if you can select an industry in which you have both familiarity with, and a passion for, your chances of success will be significantly greater.

Finding the Right Business for You

Once you’ve decided on your sector, you'll need to draw up a shortlist of prospects. Here are some tips and tricks to help you.

Once you've decided which industry you want to enter – although you may wish to keep your options open – you'll need to draw up a shortlist of prospects. When you are buying an existing business, you will have to carefully select the one that is right for you.

We explain the ways – such as price, location and owner-financed opportunities – to drill down the businesses that suit your circumstances.

Once you’ve found the business you like, you can submit inquiries to the owners to find out more.

If you’ve already decided which sector to buy your business in – or you may still be open-minded – now, it’s time to narrow your search further. When you’re browsing businesses for sale the choice can be overwhelming – running into thousands of, say, restaurants for sale!

Search filters

Looking through BusinessesForSale.com can give you thousands of results of businesses for sale. That is why there is a search filter option so you can find the one that suits your needs perfectly.

Below are some variables by which you can filter your search for any sector you’re seeking, down to a more manageable choice.

Price

How much are you willing and able to invest and borrow in total? This will dramatically reduce your list of viable options – unless of course, you can afford even the most expensive businesses and set a floor on the price range too.

Relocatable

Perhaps you're up for relocating to anywhere in Canada or even around the world. Bear in mind there is also a filter for relocatable businesses.

Sales revenue or cash flow

You can also filter results by key financials. You will need to make sure you can get a good return on your investment.

Age of listing and price reduced

The longer a business has been on the market, the keener (perhaps desperate) the seller might be to sell up and therefore be more willing to compromise. Similarly, price-reduced businesses indicate that sellers are struggling to find a buyer, often because they’ve overpriced the business – although they may simply be keen for a quick sale.

However, while these filters could be a route to a bargain, some buyers can be put off by a business that potentially, no one seems to want.

Leasehold or freehold property

If you buy the property outright, you’ll be unburdened thereafter by rent payments – but you are adding a significant premium to the asking price.

Franchise

A franchise resale means that you buy into an established brand and receive training and ongoing support.

It also buys you a tried-and-tested formula – although this is a negative if you want complete entrepreneurial freedom.

In receivership or administration

An appealing option if your budget is tight and/or you like a challenge. But don’t fool yourself – it will be an enormous challenge!

Owner financed

This means the seller is willing to part-finance the deal – in other words, accept a portion of the asking price in instalments.

This stretches your budget further and shows that the seller trusts that their business will thrive in your hands as they know that you’ll be able to fulfil your repayments.

Accommodation included

Do you want to live where you work?

It cuts out commuting costs and time (a valuable asset for an entrepreneur). It also bumps up the price significantly – although it usually gives you more spending power if you have an existing home to sell first. Particularly common in sectors like B&Bs, farms, and retailers.

Miscellaneous filters

You can also narrow your search down to family-run businesses; those you can operate from home (often websites), midmarket businesses and 'unique' businesses.

Once you've found a business - or several businesses - that you like, then you can submit inquiries to the owners - free of charge - to find out more and perhaps arrange negotiations.

Find out more: Want to know more about the buy-side of M&A? Understand the buyer’s perspective in mergers and acquisitions.

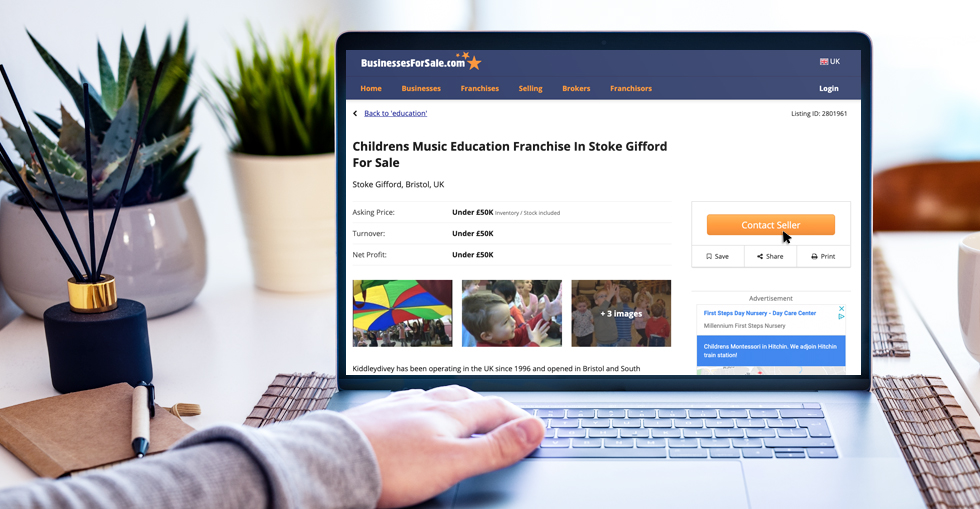

Making Online inquiries on a Business for Sale

How to establish if the business is right for you and how to convince the seller that you’re right for the business.

Have you decided to buy a business, chosen your sector and narrowed the choice down to one or a few businesses for sale that interest you?

Through BusinessesForSale.com you can submit online inquiries to the existing owners expressing your interest.

But once you’ve decided to buy a business and you’ve found one or a few for sale that interest you, you can submit inquiries to the existing owners for further information.

You can do this free of charge by clicking on the orange ‘contact seller’ button on the business listing. However, as a premium (paying) buyer you’ll get additional benefits like priority customer support and getting your inquiries prioritised in the seller's inbox.

The aim of online inquiries

You should make inquiries with two goals in mind. One is to find out more about the business to decide if you want to take your interest further. And if the seller is to agree to formal negotiations, then you also need to convince them that your interest is sincere and credible.

Many sellers have an emotional investment in the business and will care about its fortunes after selling up. Therefore, evidence of your suitability – in terms of skills, experience and attitude – may convince the buyer to open negotiations with you over other interested parties.

Don’t be a tyre kicker

Sellers often deal with inquirers who show initial interest only to back off after several email exchanges or phone calls. Frustrated at the time wasted, they’ll be vigilant for tell-tale signs that you’re a ‘tyre kicker’.

Show them that you understand and have researched the sector and don’t be afraid to ask questions. Show them that you’re a determined and committed buyer so you’re not overlooked among the mass of inquiries they may receive.

Firming up or cooling your interest

Don’t expect sellers to provide detailed or confidential information until they’re convinced that you’re a serious buyer. And even then, you probably won’t see any financial documents until you’ve signed a non-disclosure agreement.

You might seek to find out more about information in the advert that either piques your interest or causes you concern. Or you might seek information that isn’t mentioned at all. Here are some questions you might pose:

- What's the history of the business?

- How long have you been running the business?

- Why are you selling the business now?

- Can you tell me more about the business model?

- What were the annual gross revenues or net profits for the past 2-3 years?

- How did you value the business? Was it valued by an independent, suitably qualified expert?

- How flexible are you on the asking price?

- What is the business's goodwill value?

- What assets and liabilities (debts) are included in the asking price?

- How would you like to structure the sale?

- Is seller financing available, and if so, how much and under what terms? Seller financing, which suggests the seller has faith in both the business and the buyer, usually covers about 10-25% of the price

- Are you willing to wait while I find external financing?

Show them the money

The seller will want to see that you have a realistic idea about how you might pay for the business, most likely through a bank loan and with enough personal funds for a down payment. But they’ll also want to see that you have a sincere interest in the business and a passion for the sector.

The seller has probably put a lot of hard work into the business over the years and they’ll want reassurance that the business will be in capable hands when they hand over the reins.

There may be clues in the ad as to what they want in a buyer – for instance, the business might be described as suiting “someone with extensive experience” in the trade.

Failing that, imagine what you’d want from a buyer if you were the seller. Sellers who care deeply about their legacy will appreciate signs that you fit their criteria.

If online inquiries proceed successfully, you’ll then move on to face-to-face negotiations, possibly through intermediaries like business brokers, and – if you haven’t already – raising finance to pay for the business.

Raising Finance to Buy a Business

It doesn’t have to be a bank loan: a guide to the financing options available –their pros, cons and typical applications –when buying a business

Most small-business acquisitions involve a bank loan, but there are alternatives.

This is a guide to the financing options available – the pros, cons and typical applications – when buying a business.

We explore debt financing, including not just bank loans but loans effectively provided by the seller, as well as equity financing, where investors buy a stake in the business.

When you inquire on a business for sale and firm up your interest, the seller will want evidence that you’ve a realistic plan for paying for the business. The most obvious method, of course, is a straightforward bank loan – but there are alternatives.

Your personal circumstances, as well as the nature of the business for sale, will influence which options are available and most suitable.

If you can afford to buy the business outright without borrowing or outside investment, even better – then you won’t need to sacrifice a share of profits to investors or loan repayments.

Debt financing

A commercial loan, also provided by building societies or credit unions, is a form of debt financing. Individuals or businesses borrow money from a lender, then repay the borrowed amount with interest, within a specified time frame.

Interest rates, repayment periods and other terms vary depending on the lender and how risky a proposition you’re seen as. You can secure more favourable terms by securing the loan against any assets you own, usually a house.

The more finance you can contribute from personal savings, the more you can probably borrow.

Tightening your belt and getting down to saving is therefore often the best way to increase your budget.

It's also worth looking into whether the interest and charges on your loan are tax-deductible – this is possible in many cases.

The great thing about debt financing is that – in contrast with equity financing – you own the business outright.

A gap between what the buyer can afford and the price the vendor is willing to accept can be bridged by vendor financing. Also known as owner or seller financing, this is where the seller effectively accepts an IOU from you, the buyer.

As with a bank loan, the buyer puts down a deposit and pays the rest, plus interest in instalments, with the business serving as collateral – i.e. the buyer regains control of the business if payments are missed.

Vendor financing can be structured as equity too, although an interest-bearing loan is more common.

The terms, which are documented in a promissory note, are agreed during negotiations on how to structure the deal.

Equity financing

Providers of equity financing invest cash in return for a stake in the business, rather than repayment of the sum lent plus interest.

Investors

Angel investors are wealthy individual investors who might be proactive in offering advice and connecting you with their network of contacts. Venture capital firms, meanwhile, typically invest larger sums than angel investors, often in high tech companies with enormous growth potential.

Taking the equity financing route means you won’t be burdened with debt or have to put your personal assets at risk. And an investor with a background in the sector can give you invaluable access to a wealth of knowledge, experience and contacts.

However, unlike debt financing, these investors then own a stake in your business, take a share of the profits and have a say in decision-making.

Friends and family

Your close ones might be willing to lend you cash or buy a stake in the business – or they may even give you the money as a gift.

But while we can expect friends and relatives to offer the best terms and be most forgiving of late repayments, they represent a double-edged sword. If you struggle to meet repayments or their investment turns sour, it can affect your personal relationships and cause rifts.

If you do borrow money from friends or family, make sure that they clearly understand the risk they’re taking from the outset.

Find out more: Looking for funding? Read our loans to buy a business guide for helpful tips and funding options.

Negotiating Terms to Buy a Business

Negotiating the terms of a business sale isn’t like a poker game where the winner takes all.

Negotiating a business purchase isn’t a zero-sum game where the winner takes all.

Compromise and mutual trust are the twin pillars that get deals over the line. Among other things, we explore the value of appointing an independent intermediary and outline six key negotiating tips for securing the best deal possible.

Once you’ve decided on a business you want to buy and the seller has deemed you a credible buyer, it’s time to come to the table ready to negotiate terms.

With this in mind, there are plenty of things to consider throughout the process.

Should I appoint a business broker?

Not every business buyer appoints a business broker to help them. But seeking professional support is something you’ll need to consider if you want help preparing for, conducting, and negotiating a business purchase.

The vendor is likely to have a professional adviser present too – possibly even conducting negotiations on their behalf.

Independent and experienced in business sales, they act as an honest broker to keep high-stake negotiations amicable, professional and moving along to a satisfying conclusion for both parties.

What does the seller want?

Take a moment to step into the seller’s shoes and consider what their ideal outcome would be.

They may make this easy for you and be upfront early on about what they want. However, others may hold their cards closer to their chest.

Knowing what they want from the negotiation will help you meet them halfway and think of various ways to structure a deal that appeals to both parties.

Above all, the seller wants to be able to trust you. Show the seller that you are trustworthy and sincere in your interest in a business they have worked so hard to build.

Never make the seller feel like you are trying to cheat them out of a fair deal; be upfront and honest about what you want and the chances of them returning the favour will rise.

What do you want?

Decide on your ideal outcome from the outset and come to the negotiation table over-prepared to discuss every possible option.

Be willing to compromise, but also to stand firm if the seller wants to cross certain ‘red lines’. For instance, you may decide the business is heavily reliant on the outgoing owner and insist that he or she continues working for the business for a limited, transitional period post-sale.

Striking the right balance is tricky - you don’t want to back down too easily, but you shouldn’t appear stubbornly resistant to compromise.

A confrontational approach rarely helps to build trust and as many sellers don’t want to surrender their business, they’ll probably avoid an emotional attachment to someone they dislike.

Being too eager to please however, will hand all the power to the seller, leaving you wide open to being ripped off and ultimately unhappy with the final outcome.

Be assertive without being aggressive. And friendly without being submissive.

Make your position clear and ask the seller to do likewise. If both parties understand the other’s goals, you can quickly reach a compromise that is fair to both of you.

There is a saying in sales, “price is only an issue in the absence of value” and I believe it rings true in negotiations too. I have successfully negotiated deals for both myself and clients that have been well under asking price and the secret is simple, provide VALUE. Now, what is value? Value is not necessarily cash and is as unique as each person in the negotiation. If you really want to win a negotiation, take the time to sit down with the people across the table from you and learn a little about them. You can achieve your goals by helping them achieve theirs. It’s that simple.

What if the seller is being unreasonable?

If you’re not prepared to walk away from the deal, then the seller has all the leverage.

If you give the impression that they needn’t compromise to make the sale happen, then you might end up with a deal that unfairly favours the seller.

So, no matter how long and tortuous the negotiations, and however much you want the business, be prepared to walk away – and make sure the seller knows this.

Remember, there’s no need to rush things.

It is worth a few more days or weeks of negotiations versus months of regret and a less healthy bank account if you hastily accept a poor deal.

A successful negotiation is all about going back and forth until both parties are happy.

Top negotiation tips in brief

- Come to the negotiating table prepared

- Take the time to walk in the seller's shoes - find out what they want from the deal

- Decide what you want from the deal - and be clear and upfront about your goals

- Mutual trust is everything

- Be assertive but not confrontational, friendly and flexible but not too accommodating

-

Be prepared to walk away if the seller won’t compromise

Once provisional terms are agreed, it’s time to check that the basis for the agreement is sound.

Negotiating in the minds of most business buyers means getting the best deal possible from a financial and potential return standpoint. Instead, a better way to think of negotiating a deal is to think about how and what terms and conditions will assure the highest likelihood of the business being successful in the future. Some of the main considerations when negotiating a deal, therefore, should be focused on assuring that employees, management, former ownership, etc. are motivated and incentivized in making the business a success post-acquisition.

Quite often we see terms that are favorable to the buyer but might have an adverse effect on the business long term as they do not provide enough incentive to some of the other stakeholders of the business. Bonus based payments and earnouts are an excellent way to assure such alignment and increasing (not decreasing) compensation packages and perks usually have a surprisingly positive effect on business performance.

Due Diligence

Once provisional terms are agreed, it’s time to check that the basis for the agreement is sound.

Conducting due diligence when buying a business is all about making sure you know exactly what you’re getting yourself into.

Taking place after terms have been agreed, due diligence is your chance to closely examine the business to authenticate claims made by the seller about the business. If you discover previously undisclosed problems, you may wish to renegotiate terms or walk away from the deal.

It’s a considerable undertaking and one you shouldn’t begin without the help of an accountant, solicitor and/or business broker.

Be as thorough as possible – otherwise you may discover proverbial skeletons in the closet only when it’s too late.

There are three main areas to focus on when you perform due diligence so you can find out what the business is worth.

The key to due diligence is your team. If you’re wondering what team I’m referring to, I mean your professional team, your Lawyer, Accountant, Mentor or Subject Matter Expert. If you’re looking to purchase a business, I highly recommend putting some time aside to source out these working professionals and developing a relationship with them. That way they understand your situation and can act fast if a deal comes up.

Commercial due diligence

The commercial part focuses on operations and the business’s place in its market: how things work day to day; typical customers and how they perceive the business; market size, growth and trends; and so on.

This is your chance to get to know the market you’re entering, business processes and the perspectives of employees, customers and suppliers.

As well as verifying that you’re buying the business you thought you were buying, it’s a great chance to familiarise yourself with how the business functions before you take over.

Commercial due diligence checklist

- Market size, growth, relevant trends

- Stock and inventory

- Perceptions of customers, suppliers and employees

- Systems and processes

- Products and services

Financial due diligence

The most important financial consideration is finding a clear paper trail. If there are financial transactions or processes that haven’t been recorded by the current owner, you could encounter problems further down the track.

If something doesn’t sit right, be upfront and ask the seller what their plan is to remedy any discrepancies before you take over the business.

Financial due diligence checklist

Here we give you a list that will help you know what to look for in financial statements when purchasing a business.

- Past, present and projected financial performance

- Business maintainable earnings (BME)

- Debtors

- Creditors

- Salaries and wages

- Insurance

- Bonds and guarantees

Legal due diligence

The legal side of due diligence is arguably the trickiest to understand, with arcane terminology and obscure technicalities to get your head around. But that’s what solicitors are for; proceeding without professional help could cause major headaches later on.

Legal proceedings are not unheard of in business and it’s not necessarily a ‘red flag’ if the business has some legal issues in its past – or even if proceedings are ongoing.

But alarm bells should ring if the seller fails to disclose these problems. It’s up to you to do the legwork and uncover anything lurking in the shadows, so that you don’t take on legal problems not of your making.

Legal due diligence checklist

- Trademarks and business names

- Legal claims and risks

- Past, present or potential liabilities

- Contract terms

- Patents

- Claims and warranties

-

Employee entitlements

The current owner will expect you to conduct due diligence and should be ready for you to talk to customers, employees, and suppliers, as well as investigate the business’s history and financials. Don’t hold back – ask all the questions you need to, get everything in writing and understand exactly what you’re getting into.

If you’re satisfied with your findings, you’re nearly there – now it’s time to close the deal.

When purchasing a business, it is of paramount importance to conduct proper and extensive due diligence. While most buyers and their advisors are focused on historic financial performance and general administrative and legal matters, looking into future business and industry trends and performance is often overlooked.

While looking back in time is a must when buying a business, it is equally important thoroughly looking forward and assuring that the type of business and its market niche have a long enough runway in order to pay off for the investment made in purchasing it.

While always difficult to predict the future, some of the questions buyers need to ask include:

- what are the biggest threats for the business

- what is the total industry market size and the particular business share of it

- what does the employee base look like and how likely it is they will remain with the business

- how "sticky" is the business and its customers and sales

- what does the competitive landscape look like

Closing the Deal

Negotiations can stall and even collapse, even at the very last minute. How do you get the deal over the line and when should you consider walking away?

Closing the deal is the final and most exciting step of all. You are now extremely close to becoming a small business owner.

After all the negotiations and trawling through so much documentation, you’re nearly ready to get the keys to your new premises.

But there can be last-minute hitches. Rarely, the deal can even collapse just when a deal seemed close.

So how do you prevent the deal from slipping through your fingers – and is it ever wise to walk away at such an advanced stage?

Bringing it all together

There are a few things to remember as you try to finalise the purchase:

Set a firm time period

There is nothing more frustrating than a deal that drags on for months on end.

Make it clear to the seller that you would like to finalise everything by a certain date – although be flexible, within reason, as to what that date should be. This reduces the risk of things drifting – there’s nothing like a deadline to inject urgency into proceedings.

Keep things moving forward

Unless there is a reasonable explanation for any delay, don’t let the process stall. Never think you’re being too pushy by reminding the buyer of an impending deadline.

Keep building trust

Don’t do anything to damage the trust you’ve built throughout the process. Until the final contract is signed, the seller can still back out.

Think before you speak

By this point, you are probably well acquainted with the seller – but keep things professional and follow best practice, under the instruction of any advisers you’ve appointed.

Don’t be afraid to ask questions

By now, you may feel like you’ve asked so many questions that there can’t possibly be anything left to ask. But if you have any doubts at all, don’t be afraid to ask for clarification on any issue, big or small – buying a business is too big a commitment not to.

Look out for warning signs

Until the final sale agreement is signed, you should always be prepared to walk away – no matter how many months you’ve invested in the process, and however much you’ve set your heart on the business.

If something doesn’t smell right, then you should at least reconsider your commitment to proceed.

Here are some due diligence problems that should prompt a rethink:

The finances aren’t adding up

Make sure your accountant checks, double checks and triple checks every piece of financial information you are given to ensure everything adds up. If it doesn’t, don’t be afraid to ask enough questions to get the answers you need.

The seller isn’t willing to renegotiate

The seller isn’t willing to compromise on the price and other terms despite due diligence having uncovered some serious, hitherto undeclared problems.

Something just doesn’t feel right

Sometimes our gut instinct tells us something isn’t right. If something feels off, even if you can’t pinpoint it, you’re not obliged to close the deal – however much that might infuriate the vendor.

If things proceed smoothly, your solicitor or broker can help you finalise and sign the sale agreement – at which point you become the legal owner of the business!